Login

Login

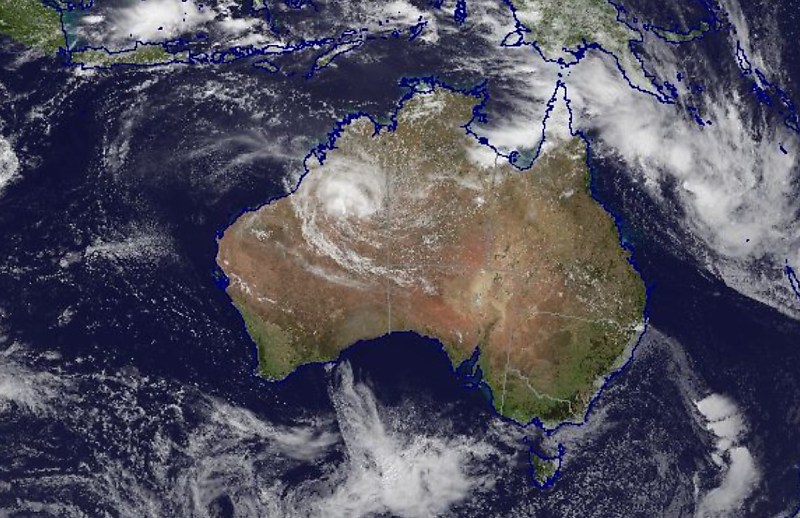

Recent natural disasters highlight the need to prepare for the worst, ASBFEO says.

Recent natural disasters highlight the need to prepare for the worst, ASBFEO says.

Three out of four small businesses lack contingency plans for a natural disaster despite storms across the country showing just how vulnerable they can be, the sector ombudsman says.

Australian Small Business and Family Enterprise Ombudsman Bruce Billson said the cyclone threats in Queensland and Northern Territory floods should be a warning of how quickly devastation could strike.

“An inquiry by my office found only one in four small businesses have a current business continuity plan,” Mr Billson said.

“Natural disasters can be devastating for small and family businesses – either their business is directly damaged or wiped out, or they are an indirect victim who has survived the disaster only to have no customers because of the impact on their town or region.

“Taking simple steps to be better prepared, sensible risk mitigation action and bolstering resilience can help small and family businesses to get back on their feet quicker.”

Mr Billson said small business owners were often the first to volunteer to help in disaster situations and it was vital they were prepared as well.

“I urge small and family businesses to be as prepared as possible and to be best placed to respond and recover. This can be as simple as ensuring your record keeping is up to date and that critical information is at hand and, where possible, digitised so you can retrieve it if your business is destroyed.”

ASBFEO said business owners should ask themselves the following questions:

ASBFEO has recommended the creation of an opt-in My Business Record to allow a small business to digitally store all relevant government-held and other vital information it might need after a disaster.

“It is clear from our work that preparation is key to small and family businesses building resilience and coming through natural disasters in the best possible shape,” Mr Billson said.

“It is equally clear the small business community cannot do this on their own and when a natural disaster strikes, certainty of response and certainty of support must be provided.

“By this we mean small business owners should automatically be engaged in local place-based planning and support services and be elevated and ‘front of mind’ in disaster response, recovery and funding arrangements. This must include indirectly affected businesses.

“We believe a business hub should be established to provide a single point from which to seek help from government and non-government agencies. And we strongly recommend a “tell-us-once” triage system should be adopted to save small business owners the trauma and time associated with repeating their story.”

Mr Billson said government grant recipients should be given additional funds for a business health check six to nine months after the original event.

“We also need an integrated response to disaster risk management for identified disaster prone areas that incorporates priority access to mitigation expenditure, co-ordinated planning across levels of government, infrastructure hardening, interest-free loans for asset and activity protection and relocation schemes, and possible use of a dedicated reinsurance vehicle.”

Mr Billson said an ongoing problem was that many small businesses were unable to secure appropriate insurance at an affordable price.

“If they can get insurance, it can come with excesses that would preclude any claim ever being made,’ he said.

“Frustratingly, insurers are also uninterested in the steps individual small and family businesses take to mitigate disaster risk, or dismissive of them.

“We have examples of individual businesses doing everything they can possibly do but it has zero impact on the availability and the pricing of their premiums.

“We’re told this is because the insurance companies look at risk across a broader pool – it is community-wide or industry-wide or neighbourhood-wide analysis. Yet the narrative, amplified through advertising, is often about what individuals might do.

“Many small and family businesses are individually doing what’s being asked of them but are seeing no upside to pricing premiums and availability and affordability of insurance cover. What might be for some an insurance ‘gap’ is too often a ‘gorge’ for small business that too many can’t cross.

“The insurance sector needs to do better – and do it now.”

Get breaking news