Login

Login

Confronted with “significant financial stress”, more individuals will find themselves in bankruptcy says AFSA.

Confronted with “significant financial stress”, more individuals will find themselves in bankruptcy says AFSA.

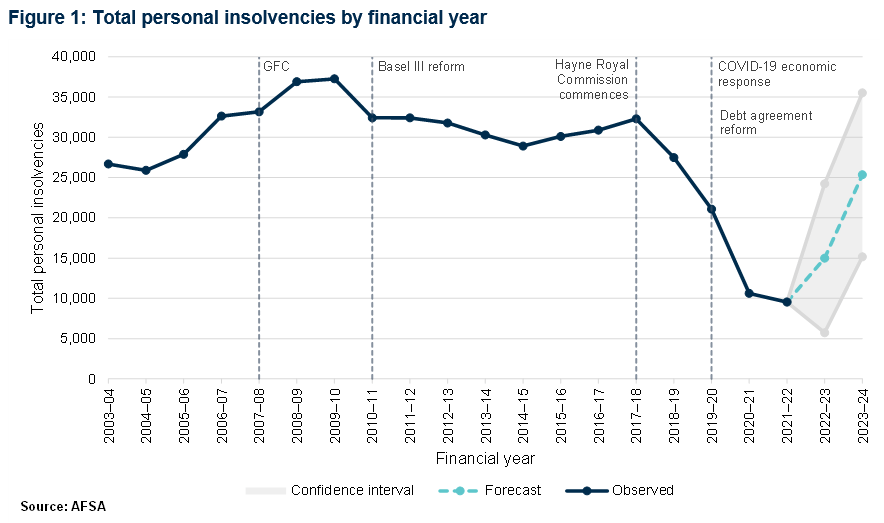

Personal insolvencies are on a path back to pre-pandemic levels driven by inflation and rising interest rates, according to data released by the Australian Financial Security Authority.

Its latest report expected personal insolvencies to rise steeply rise towards the 10-year average of 25,300 over the next two years, from a historically low base of 9,545 in 2021-22 due to special measures under COVID.

“Challenges like rising interest rates and high inflation are putting many people under significant financial stress,” AFSA chief executive Tim Beresford said.

“AFSA supports the flow of Australia’s $3.5 trillion credit system by allowing people in financial distress to get a fresh start, while providing a remedy for those who are owed money.”

The State of the Personal Insolvency System report pointed to danger signs including:

“Australian households are currently experiencing financial stress,” the report said. “Unemployment remains low but the risk of insolvency is rising as household saving buffers decline and cost of living pressures increase. Other adverse macro-economic factors such as rising interest rates, high inflation, ongoing supply chain pressures and rising energy prices will put those vulnerable under more financial stress.”

The report found most people who entered personal insolvency during 2021-22 had low levels of debt, with 52.7 per cent involving less than $50,000 in liabilities and just over a quarter of totalling more than $100,000.

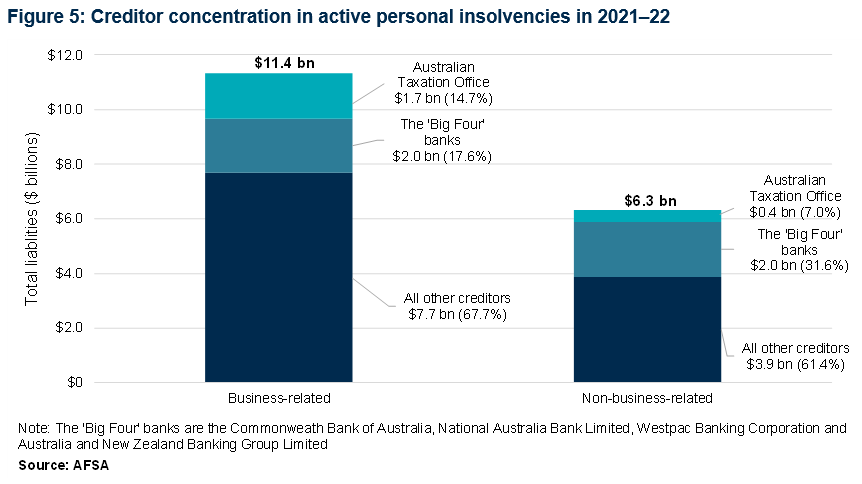

Total liabilities amounted to almost $18 billion, with major creditors the ATO owed $2.1 billion and the big four banks $4 billion.

Business-related personal insolvencies accounted for almost two-thirds of the liabilities, at $11.4 billion. The average debt for a business-related personal insolvency was $830,502 – almost six times that of a non-business-related personal insolvency ($141,733).

The report said the AFSA was “broadening our regulatory toolkit to respond to new and emerging harms, combining our regulatory expertise, market surveillance and data analytics to balance the interests of debtors, practitioners and creditors, and deliver firm and fair outcomes for Australians”.

Mr Beresford expected many of the issues to be explored at an upcoming personal insolvency roundtable in March.

“We are aware that many of our stakeholders are interested in potential personal insolvency reforms,” he said. “The government is keen to explore pressure points of the current personal insolvency system, critical reform areas and longer-term priorities.”

Get breaking news